International Payment Solutions Enhancing Access to Licensed Digital Gaming Environments

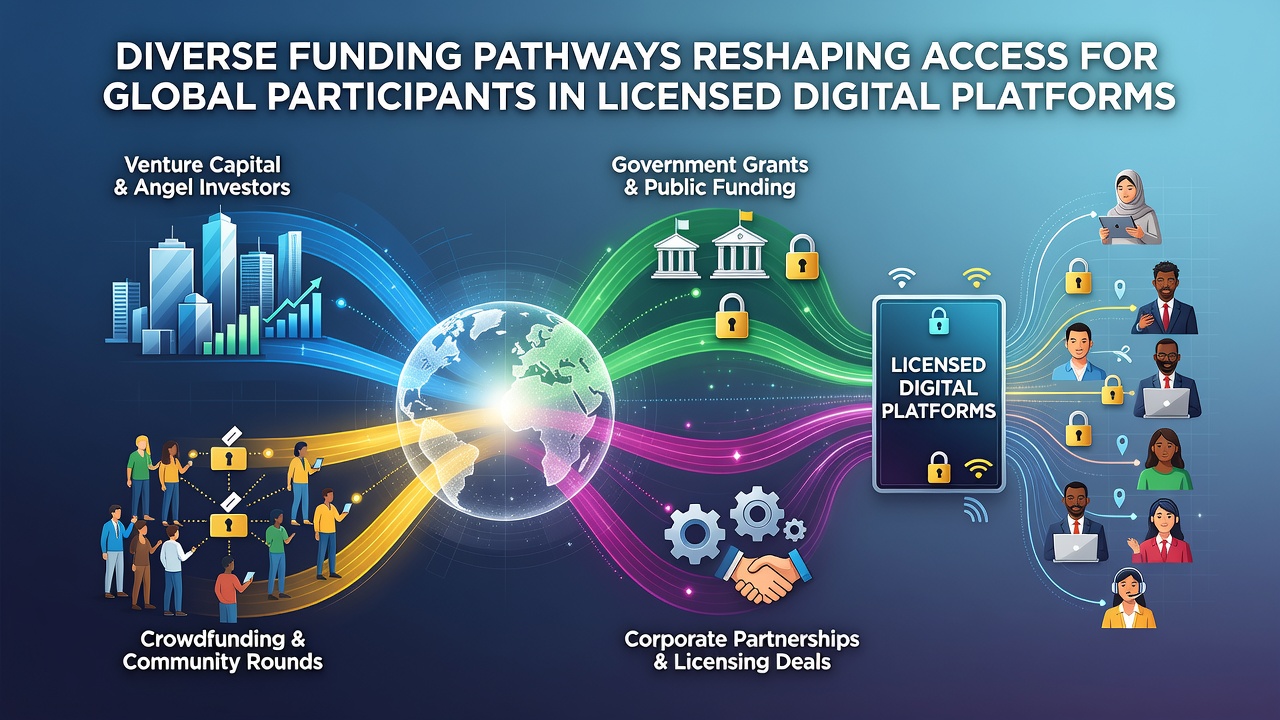

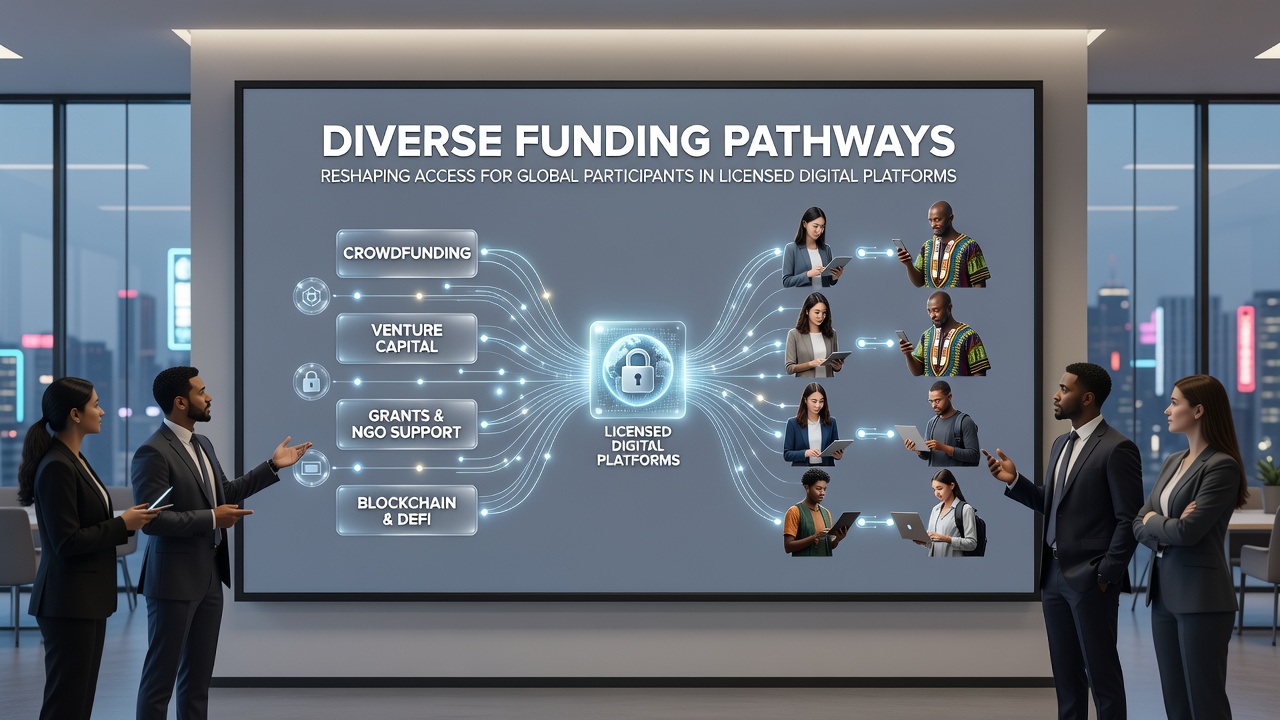

Payment diversity has become a central factor in how licensed digital platforms reach participants across borders, and data from multiple regulatory bodies shows steady expansion in options that comply with local rules while serving users in different regions. Credit cards, bank transfers, e-wallets, mobile billing and cryptocurrencies now operate alongside one another in many jurisdictions, each pathway carrying its own verification steps and fee structures that platforms must balance against compliance requirements.

Regional Regulatory Frameworks Shaping Funding Options

Authorities in North America, Europe and Asia-Pacific maintain distinct licensing conditions that dictate which funding methods platforms can offer, and operators adjust their systems accordingly to remain within approved boundaries. The Nevada Gaming Control Board, for instance, requires strict transaction logging for all deposits and withdrawals on platforms it oversees, while Australian state regulators emphasize consumer protection measures that include spending limits tied to verified payment accounts. These frameworks have led platforms to integrate multiple rails rather than rely on a single method, because participants from one country often face restrictions that do not apply elsewhere.

Observers note that when a platform adds an approved e-wallet or local bank integration, participation from that region frequently rises within weeks, according to figures shared by industry associations tracking licensed activity. Such growth occurs because users gain a familiar and regulated route that bypasses previous barriers such as currency conversion friction or lengthy manual reviews.

Technology Behind Multi-Rail Funding Systems

Modern platforms rely on layered verification technology that processes each funding type through separate compliance checks before funds reach the user account, and this architecture allows simultaneous support for traditional cards, instant bank transfers and digital assets. Developers design these systems to flag anomalies in real time, routing higher-risk transactions through additional review layers while permitting low-risk ones to clear quickly. The result is a network where speed and security operate in tandem rather than in opposition.

Researchers at several universities have examined how these multi-rail systems reduce friction for cross-border users, and their analyses indicate that platforms offering at least four distinct approved methods record higher retention rates from international traffic. One study published in 2025 highlighted that cryptocurrency rails, when licensed and monitored, provide settlement times measured in minutes rather than days, which aligns with user expectations formed by everyday digital commerce.

June 2026 Developments in Payment Integration

By June 2026 several platforms had completed updates that embedded new regional payment schemes into their existing infrastructure, and reports from trade groups documented corresponding increases in verified accounts from previously underserved markets. These updates followed policy clarifications issued earlier in the year by bodies outside the United Kingdom, including updates from the Malta Gaming Authority and the New Jersey Division of Gaming Enforcement that clarified acceptable documentation for digital asset deposits. Participants gained access through combinations of local bank APIs and regulated stablecoin channels, each verified against sanction lists and anti-money-laundering databases before activation.

Industry organizations tracking licensed activity have recorded that platforms maintaining diversified funding portfolios experience fewer interruptions when individual rails encounter temporary regulatory reviews, because traffic simply shifts to remaining approved pathways until the issue resolves. This redundancy has become a practical necessity rather than an optional feature in an environment where rules evolve at different speeds across jurisdictions.

Conclusion

The expansion of compliant funding pathways continues to alter how global participants reach licensed digital platforms, with each new integration reflecting both technological capability and regulatory alignment. Data from varied oversight bodies shows measurable shifts in participation patterns once additional rails become available, and ongoing refinements in verification technology support the maintenance of security standards while serving wider audiences. These developments remain grounded in jurisdiction-specific requirements that platforms must satisfy to operate legally across multiple regions.